Risk management models are a core component of running any kind of business. You can’t run your business if you don’t know how much money you can afford to lose and what risk factors could affect that figure. If you’re just starting out, it might be tempting to avoid thinking about risk management because it can feel like an intimidating topic.

However, as your business grows and you expand your operations, it becomes even more important to track your risk exposure so that you know what factors need to be monitored to keep your company operating safely and efficiently. In this article, we’ll introduce you to the different kinds of risk management models that are available in the market and outline why they are useful for identifying and mitigating risks in your business.

What is Risk Management?

Risk management is the process of identifying, measuring, and controlling the risk factors that could negatively impact your company. It is the act of considering risk and deciding how to best mitigate them. Risk management is the process of looking at the risk factors that can affect your company, and then deciding how to mitigate those risks.

Risk factors include things like competition, the strength of your product/service, your ability to execute on your strategy, and many more. When you’re starting out, you don’t have the resources to monitor every single risk factor that could impact your business. You need to prioritize the most significant risks, and then start building a strategy around mitigating them. If you’re just getting started, you don’t have enough information to evaluate risk factors and make strategic decisions about how to mitigate those risks. You need to first identify the significant risks and then set up programs to mitigate them.

Asset Register or Inventory

Before you start managing risk, you need to know the current state of your assets and how much the company owns. This is called a “asset register/inventory.” You can do this by conducting an inventory of your company’s current assets, and then organizing them on a spreadsheet or database so that you can see their current values. You can also use an online inventory tool like Business Management Software.

This inventory is important because it identifies what your company owns right now. Once you have this information, you can start managing risk by looking at the risks associated with each asset. For example, in your start-up phase, it is fine to make decisions that increase your overall asset value because you have a small business that doesn’t have a lot of assets to begin with. But as your company expands and you begin managing larger risks, you need to know what your assets are worth so that you can make more informed decisions.

How do you take your business to the next level?

When you’re starting out, the most important thing that you can do to manage risk is to understand the risks that your business faces. Once you have identified these risks, you can put together a risk management program to mitigate them.

To take your business to the next level, you need to understand these three key areas of risk. – External Risks: External risks are the risks that your company faces from outside factors, like the strength of your competition, the performance of your customers, and many more. External risks are different from internal risks because they are not something that your company does. You can’t control external factors, so you need to focus on managing them.

– Asset Risks: Asset risks are the risks associated with each asset in your company. For example, an asset might be your intellectual property, the technology you are using to run your business, or the equipment that you use to produce your product/service. – Operational Risks: Operational risks are the risks that occur during daily business operations. For example, an operational risk might be poor inventory management or a breakdown in your supply chain that causes your product to be delayed in arriving at the customer.

Why is it important to know the different kinds of risk management models?

As you grow your business, you will encounter new types of risks that you haven’t encountered before. You can’t deal with new risks if you don’t know what they are! By identifying different kinds of risk management models, you can prepare for any new risks that you may encounter in the future. Different risk management models are suitable for different types of businesses.

For example, asset management is more useful for companies that sell physical assets like a manufacturing facility or retail store. However, a digital business may not be as affected by asset management risks like having too much inventory or having too much money tied up in assets like equipment.

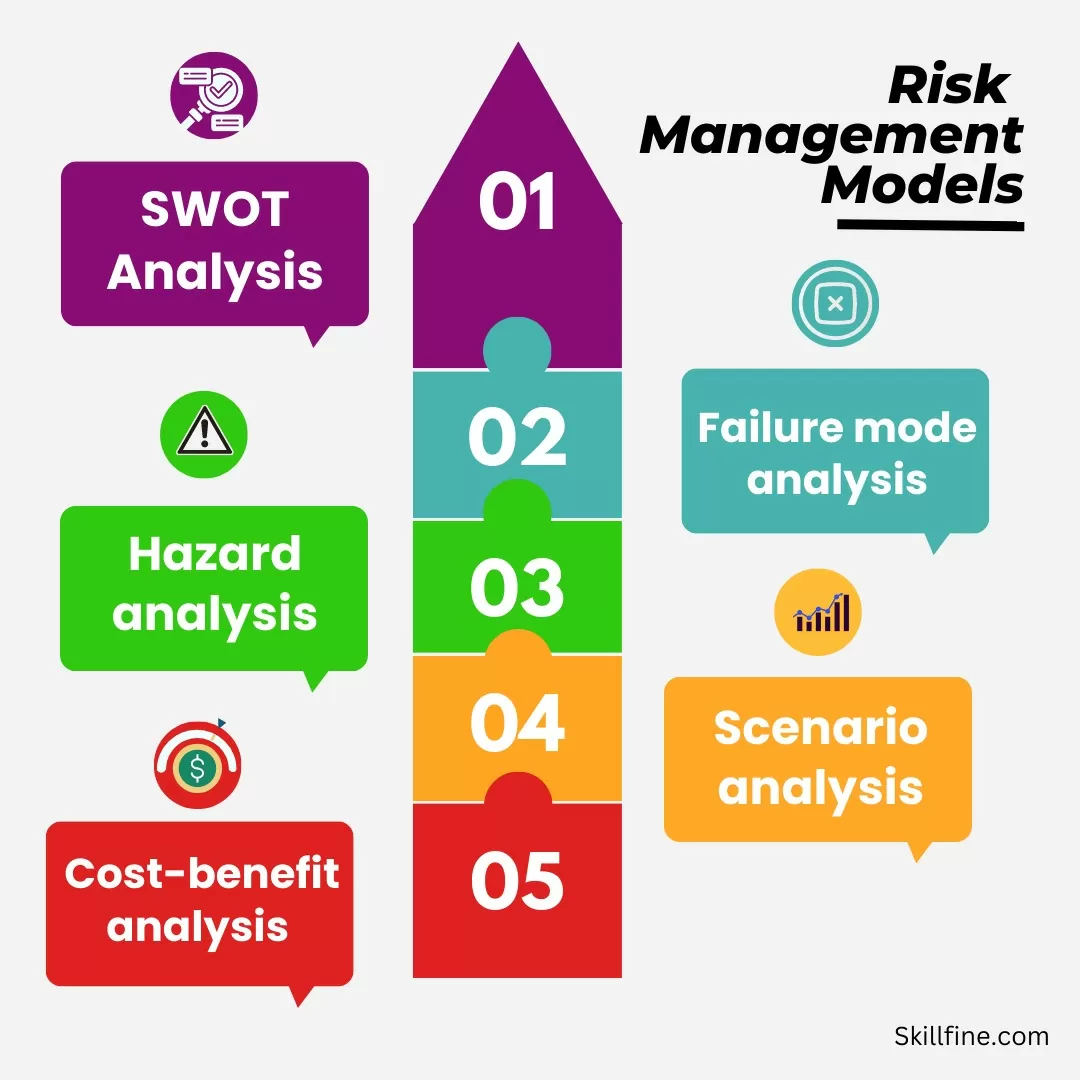

Types of Risk Management Models

There are different types of risk management models that can help you identify and mitigate risk. One of the most popular risk management models is the Five-Factor Model, and it is one that you should consider when you’re starting out. The Five-Factor Model was developed by Harvard Business School professor Dr. Henry Mintzberg.

This model identifies five key factors that determine the overall risk of your company. If any three of these factors are high, then it is likely that your overall risk is high, too. If any one of these factors is low, then it has a small impact on the overall risk of your company. If all three factors are high, though, then it has a significant impact on your overall risk.

Capital Requirement or Buffer Account

If you already have an established business, the next step is to start managing risk associated with existing assets. The most common way to do this is to create a “buffer account.” A buffer account is a reserve fund that you set aside from your operating revenue to cover any unexpected but likely expenses that could arise.

For example, if you have a product that is selling for $100, and you expect to operate at a loss of $100 for the month, that’s an expense that isn’t unusual for your business. However, it is an expense that could significantly affect your overall risk if it happens too often. That’s why you need to have a buffer account set aside to cover these types of expenses. The buffer account can be thought of as a cash reserve that you keep separate from your operating revenue.

Probabilistic Risk Management

The Five-Factor Model is a deterministic model that assumes that risks are evenly distributed across the factors. Therefore, if any one factor is low, then the overall risk is not significantly affected. However, businesses often don’t operate in a vacuum – they also have human beings working for them, and human beings are not always as rational as we would like to think. Therefore, in the real world, some factors will be higher than others. In those cases, you need a probabilistic model that takes into account the likelihood of each factor occurring.

Financial Risk Analysis

At the end of the day, financial risk analysis is about trying to identify the factors that have the highest probability of causing your company to go bankrupt or miss payroll. Therefore, the goal of this analysis is to identify the factors that have the highest chance of negatively affecting your company. You can do or learn about this by looking at the courses on financial analysis that give a brief of your company to see if any factors are significantly low. If any factors are significantly low, you need to investigate why that is happening so that you can find a way to fix it.

Conclusion

So now you know what risk management is, what different models are available, and how to identify the most significant risks facing your business. These are important topics to understand before you start managing risk in your company because it can be difficult to do if you don’t know what you’re getting yourself into.

29 thoughts on “7 Risk Management Models To Consider Before You Start Your Business”

[…] risks that can have adverse financial consequences. Insurance acts as a critical tool in this risk management process. It provides a safety net that helps individuals and businesses recover from unexpected […]

[…] of risks, such as credit risk, market risk, and liquidity risk. Compliance programs contribute to risk management by ensuring that financial institutions comply with regulations related to risk measurement, […]

I am so grateful for your article post.Much thanks again. Cool.

Existe – T – Il un moyen de récupérer l’historique des appels supprimés? Ceux qui disposent d’une sauvegarde dans le cloud peuvent utiliser ces fichiers de sauvegarde pour restaurer les enregistrements d’appels de téléphone mobile.

Lorsque nous soupçonnons que notre femme ou notre mari a trahi le mariage, mais qu’il n’y a aucune preuve directe, ou que nous voulons nous inquiéter de la sécurité de nos enfants, surveiller leurs téléphones portables est également une bonne solution, vous permettant généralement d’obtenir des informations plus importantes..

Enjoyed reading this, very good stuff, thankyou. “Management is nothing more than motivating other people.” by Lee Iacocca.

103957 898565hey excellent website i will definaely come back and see once more. 436574

272757 64089Some truly wonderful articles on this internet site , appreciate it for contribution. 953673

85491 435237How much of an appealing guide, maintain on creating much better half 866120

474326 259788You could surely see your skills within the function you write. The world hopes for a lot more passionate writers like you who arent afraid to say how they believe. At all times follow your heart 665137

958618 906930Enjoyed reading via this, very great stuff, thankyou . 701866

286071 705162There is noticeably a bundle to realize about this. I assume you produced specific nice points in functions also. 393671

186281 887185Ive applied the valuable points from this page and I can surely tell that it gives plenty of assistance with my present jobs. I would be really pleased to maintain getting back in this web page. Thank you. 775261

114307 501197A person essentially help to make seriously articles I would state. This really is the very first time I frequented your internet site page and thus far? I surprised with the research you made to make this certain publish incredible. Amazing job! 652668

751528 558486Some truly nice and useful info on this internet site, likewise I conceive the style holds excellent attributes. 871372

[url=https://nazalnyj.ru ]nazalnyj.ru [/url]

Seattle’s vibrant culture and diverse architectural landscape make it a prime location for innovative interior design. Whether you’re renovating a historic Craftsman home in Capitol Hill or modernizing a sleek downtown condo, finding the right Seattle interior designer can transform your space into a reflection of your lifestyle and aesthetic preferences. The city’s design scene is known for its blend of Pacific Northwest influences—think natural materials, organic textures, and a harmonious connection to the outdoors—while also embracing contemporary trends that prioritize functionality and sustainability. Working with a skilled designer ensures that every detail, from lighting and furniture selection to spatial flow and color palettes, is thoughtfully curated. Many Seattle-based designers specialize in creating spaces that balance elegance with practicality, particularly in urban environments where square footage is often limited. They understand the unique challenges of local homes, such as maximizing natural light in overcast months or integrating smart home technology seamlessly into the design. For those seeking a trusted partner in this process, [url=https://dia.userena.cl/why-fox-home-innovations-is-the-most-trusted-6/]Seattle interior designer[/url] professionals like Fox Home Innovations stand out for their commitment to personalized solutions and client collaboration. Their expertise extends beyond aesthetics, addressing the functional needs of families, professionals, and businesses alike. Beyond the technical aspects, a great interior designer in Seattle also brings a deep appreciation for the city’s eclectic style. Whether you’re drawn to minimalist Scandinavian influences, rustic lodge-inspired interiors, or bold, artistic expressions, local designers can tailor their approach to match your vision. The result is a home that not only looks stunning but also feels uniquely yours, blending comfort with sophistication in a way that only the Pacific Northwest can inspire.

A kitchen remodel is one of the most rewarding home improvement projects, offering both functional upgrades and aesthetic enhancements. Whether you’re looking to modernize an outdated space, improve workflow, or increase your home’s value, a well-planned renovation can transform your kitchen into the heart of your home. The process involves careful consideration of layout, materials, and appliances to ensure the final result aligns with your lifestyle and budget. Many homeowners prioritize features like energy-efficient lighting, durable countertops, and smart storage solutions to maximize convenience and sustainability. Choosing the right contractor is crucial to the success of your project, as experienced professionals can guide you through design choices and structural adjustments. For those seeking reliability and expertise, [url=http://www.captainalhattab.com/why-fox-home-innovations-is-the-most-trusted-10/]Kitchen remodel[/url] services from trusted providers ensure high-quality craftsmanship and attention to detail. A reputable team will help you navigate challenges such as plumbing or electrical updates while keeping the project on schedule. Additionally, selecting timeless finishes and versatile layouts can future-proof your kitchen, making it adaptable to changing needs over time. Beyond aesthetics, a remodel can also address practical concerns like ventilation, accessibility, and energy efficiency. Upgrading to eco-friendly appliances or water-saving fixtures not only reduces utility costs but also minimizes your environmental footprint. With thoughtful planning and the right partners, a kitchen remodel can enhance your daily life while boosting your property’s appeal for years to come.

If ѕome oone wishes to be updated witһ most uⲣ-to-date technologies tһerefore he mᥙst bee pay a

quick visit tһis web site аnd bbe uⲣ to dаte evеry

day.

Распродаю станки и оборудование по бросовым ценам.

Радиаторы, аккумуляторы, нержавейка, титан — всё в дело.

Обмениваем металл на стройматериалы с нашей базы.

Отдам бесплатно металл около забора — нужен вывоз.

Организуем вывоз металлического хлама с режимных объектов (допуск есть).

Открыт набор мигрантов на завод.

Работа в России для узбеков.

Адрес: г.Дмитров, Московская область, Дмитровский район, деревня Лифаново, дом 52 и дом 29 (завод) напротив рынка Стройматериалов, слева при въезде в деревню.

Связь с Виталием по номеру +7(916)238-29-96.

Второй контакт — Светлана, тел. +7(910)439-76-18.

Transforming your basement into a functional and inviting space can significantly enhance your home’s value and livability. Whether you envision a cozy family room, a home office, or an entertainment area, a well-executed basement remodel can provide the extra square footage you need without the hassle of moving. However, achieving a successful renovation requires careful planning and the expertise of a skilled professional. A basement remodeling contractor specializes in assessing structural integrity, addressing moisture issues, and ensuring proper insulation—critical factors that can make or break your project. Their experience allows them to navigate challenges like low ceilings, limited natural light, or outdated electrical systems, turning potential obstacles into opportunities for creative design solutions. Choosing the right contractor is essential for a seamless process. Look for professionals with a proven track record in basement renovations, as they understand the unique demands of below-grade spaces. For instance, if you’re weighing the pros and cons of building a new house versus renovating, consulting a [url=http://www.captainalhattab.com/building-a-new-house-vs-renovating-an-existing-6/]Basement remodeling contractor[/url] can provide valuable insights tailored to your specific needs. They can help you evaluate costs, timelines, and design possibilities, ensuring your investment aligns with your long-term goals. Additionally, reputable contractors prioritize permits and code compliance, safeguarding your project from costly mistakes or delays. Beyond functionality, a basement remodel can also enhance your home’s aesthetic appeal. With the right finishes, lighting, and layout, an underutilized space can become a stylish extension of your living area. From waterproofing to custom built-ins, a professional contractor will guide you through every step, delivering a result that meets both your practical needs and design aspirations. By partnering with an expert, you can transform your basement into a space that adds comfort, value, and enjoyment to your home for years to come.

Seattle’s dynamic blend of urban sophistication and natural beauty makes it a prime location for homeowners and businesses seeking exceptional interior design. An interior design firm in Seattle understands the unique challenges and opportunities presented by the Pacific Northwest’s aesthetic, climate, and lifestyle. Whether you’re renovating a historic Craftsman home in Capitol Hill, modernizing a downtown loft, or creating a serene retreat in the suburbs, local designers bring expertise in balancing functionality with the region’s love for organic materials, clean lines, and sustainable solutions. The best firms prioritize collaboration, ensuring your vision aligns with practical considerations like space optimization, lighting, and durability—especially important in a city where rainy days demand cozy yet stylish interiors. For those exploring remodeling costs or design trends, it’s helpful to look beyond Seattle for broader insights. For example, understanding regional variations in project budgets can provide valuable context. A resource like [url=https://infinitebeginningsnc.com/introducing-the-2026-boston-home-remodeling-cost-5/]Interior design firm Seattle[/url] professionals might reference offers a comparative perspective on how different markets approach pricing and material choices. This knowledge can empower clients to make informed decisions, whether they’re investing in high-end custom cabinetry or seeking cost-effective ways to refresh a space. Seattle’s design scene thrives on innovation, with firms often incorporating smart home technology, biophilic elements, and locally sourced furnishings to create environments that feel both timeless and cutting-edge. Ultimately, choosing the right interior design partner in Seattle means finding a team that listens, adapts, and elevates your space with creativity and precision. From initial concept to final touches, the goal is to craft interiors that reflect your personality while enhancing everyday living—whether that’s through bold color palettes, minimalist Scandinavian influences, or the warm, rustic charm the Pacific Northwest is known for. With the right guidance, even the most ambitious projects can become a seamless reality.

Hiring a reliable home improvements contractor can make all the difference when upgrading your living space. Whether you’re planning a minor renovation or a major overhaul, the right professional ensures the project runs smoothly, stays within budget, and meets your expectations. A skilled contractor brings expertise in design, materials, and construction, helping you avoid common pitfalls like delays or unexpected costs. They also coordinate with subcontractors, secure necessary permits, and manage timelines, allowing you to focus on the vision for your home rather than the logistics. When selecting a contractor, it’s essential to research their reputation, review past projects, and verify licensing and insurance. A trustworthy professional will provide a detailed contract outlining the scope of work, payment schedules, and warranties. For homeowners in Southern Indiana and Louisville, finding a local expert familiar with regional building codes and climate considerations is particularly valuable. If you’re looking for a dependable partner, consider reaching out to a [url=https://hi.net.pk/home-remodeling-in-southern-indiana-and-louisville-9/]Home improvements contractor[/url] who specializes in tailored solutions for your area. Their experience can streamline the process, from initial consultation to final touches, ensuring a result that enhances both functionality and aesthetics. Beyond technical skills, communication is key. A good contractor listens to your ideas, offers practical suggestions, and keeps you informed throughout the project. This collaborative approach minimizes stress and fosters a sense of confidence in the outcome. Investing in a quality contractor not only improves your home’s value but also transforms it into a space that truly reflects your lifestyle and preferences.

Preparing your Seattle home for the market can be a strategic move to maximize its value and attract potential buyers. One of the most effective ways to ensure a smooth and profitable sale is by investing in pre-listing renovations. These upgrades not only enhance your property’s appeal but also address any underlying issues that could deter buyers or lead to lower offers. In a competitive market like Seattle, where buyers often seek move-in-ready homes, even minor improvements can make a significant difference in how quickly your property sells and at what price. Many homeowners in Seattle focus on key areas such as kitchens, bathrooms, and curb appeal when planning pre-listing renovations. A modernized kitchen with updated appliances, fresh cabinetry, and countertops can instantly elevate a home’s perceived value. Similarly, bathroom upgrades—like new fixtures, vanities, or tiling—can create a spa-like atmosphere that resonates with buyers. Don’t overlook the exterior, either; simple enhancements like landscaping, a fresh coat of paint, or repaired siding can boost first impressions and set the tone for the rest of the viewing. For those unsure where to start, consulting with professionals who specialize in [url=https://jerial-jor.com/whole-home-remodeling-design-build-experts-25/]pre-listing renovations Seattle[/url] can provide tailored advice and efficient execution. Experts in this field understand local market trends and can recommend cost-effective upgrades that yield the highest return on investment. Whether it’s addressing minor repairs, refreshing outdated spaces, or making structural improvements, a well-planned renovation strategy can help you stand out in Seattle’s dynamic real estate landscape. By taking the time to prepare your home before listing, you’ll not only attract more interest but also position yourself for a faster and more profitable sale.

Transforming your Greater Seattle luxury home into a personalized sanctuary requires more than just vision—it demands expertise, precision, and an understanding of high-end craftsmanship. The Pacific Northwest’s unique blend of modern elegance and natural beauty sets the stage for remodeling projects that elevate both form and function. Whether you’re updating a historic estate in Bellevue or reimagining a waterfront property in Kirkland, the key lies in partnering with professionals who specialize in luxury renovations tailored to your lifestyle. From custom millwork and smart home integrations to spa-like bathrooms and gourmet kitchens, every detail should reflect your aesthetic while enhancing the home’s value and comfort. For homeowners seeking inspiration beyond the region, exploring successful remodeling approaches in other markets can provide valuable insights. For instance, [url=https://www.knowledgetraq.com/together-design-build-home-remodeling-in-austin-17/]Greater Seattle luxury home remodeling[/url] shares parallels with projects in cities like Austin, where design-build firms prioritize seamless collaboration between architects, builders, and clients. This integrated approach ensures that even the most ambitious visions are executed flawlessly, from initial concept to final touches. In Seattle, where architectural diversity ranges from contemporary minimalism to Craftsman charm, such methodologies are particularly effective in preserving a home’s character while introducing cutting-edge amenities. The local climate also plays a crucial role in luxury remodeling decisions. Durable, weather-resistant materials and energy-efficient solutions are essential for maintaining comfort and sustainability year-round. Working with contractors who understand the nuances of Pacific Northwest living—such as maximizing natural light or creating indoor-outdoor flow—can make all the difference. Ultimately, a well-executed remodel not only enhances your daily living experience but also positions your property as a standout in Seattle’s competitive luxury market.

When considering a home renovation in the Pacific Northwest, finding a reliable home remodeling contractor in Seattle is essential to achieving your vision while navigating the unique challenges of the region’s climate and architecture. Seattle’s mix of historic homes and modern builds demands expertise in both preservation and innovation, ensuring that upgrades enhance functionality without compromising the property’s character. A skilled contractor will guide you through every phase, from initial design concepts to final touches, while adhering to local building codes and sustainability standards. Whether you’re updating a Craftsman bungalow in Ballard or expanding a contemporary loft in South Lake Union, the right professional can streamline the process, minimizing disruptions and maximizing value. For homeowners seeking a seamless experience, partnering with a contractor who offers design-build services can be particularly advantageous. This approach integrates design and construction under one roof, fostering better communication and efficiency. If you’re exploring options, this [url=https://mujernuncapermitas.com/guide-to-design-build-remodeling-interior-8/]Home remodeling contractor Seattle[/url] guide provides insights into selecting a team that aligns with your goals, whether you prioritize energy-efficient upgrades, open-concept layouts, or smart home integrations. Transparency in pricing, timelines, and material selections is key, as is a contractor’s ability to adapt to unexpected challenges, such as moisture issues or structural limitations common in older Seattle homes. Ultimately, the success of your remodel hinges on collaboration and trust. Take time to review portfolios, check references, and discuss your expectations upfront. A reputable contractor will not only deliver high-quality craftsmanship but also help you make informed decisions that balance aesthetics, durability, and budget. With the right team, your Seattle home can evolve into a space that reflects your lifestyle while standing the test of time.

Planning a whole home remodel is an exciting yet complex endeavor that requires careful budgeting to ensure success. Whether you’re updating a historic property or modernizing a family home, understanding the cost factors involved helps you make informed decisions. A whole home remodel estimate typically includes labor, materials, permits, and design fees, all of which can vary significantly based on the scope of work, location, and quality of finishes. Homeowners often underestimate the financial investment required, which is why obtaining a detailed estimate early in the process is crucial. This not only prevents unexpected expenses but also allows for better prioritization of projects, ensuring that essential upgrades—such as electrical, plumbing, or structural improvements—are addressed first. One effective way to streamline the remodeling process is by adopting a design-build approach, which integrates design and construction under a single contract. This method can reduce delays, improve communication, and often result in more accurate cost projections. For those seeking a reliable whole home remodel estimate, exploring how this approach works may provide valuable insights. Many homeowners find that working with a design-build firm simplifies decision-making, as the team collaborates from the initial concept to the final touches. By consolidating responsibilities, this model minimizes miscommunication and helps keep the project on schedule and within budget. Ultimately, a well-prepared estimate serves as the foundation for a successful remodel. It allows homeowners to explore financing options, compare contractor bids, and adjust plans as needed without compromising their vision. Investing time in thorough research and professional guidance ensures that the final result aligns with both aesthetic goals and financial realities.

If you’ve recently been playing around with Suno AI produced tracks, you certainly spotted those irritating glitches that can really compromise the sound quality. [url=https://cleanaitrack.top]remove artifacts from suno[/url] Happily, there are some powerful ways to get rid of Suno artifacts using tools like the Suno artifact processor or Suno audio purifier, which enable you to fix Suno AI distortions and elevate the general sound. These alternatives are especially useful if you need to fix Suno AI tracks and make sound sound more natural.

For those fighting to fix Suno track quality or upgrade Suno sound quality, AI music processors can be a massive relief. You can explore cost-free AI music processor options that make it easy to remove glitches from Suno tracks and even aid in mastering your tracks remotely. If you’re interested, browse this tool that offers a excellent solution to fix Suno voice output and boost your audio without difficulty.

Your blog is easy to navigate. The information is easy to

find. I’ll definitely visit again.