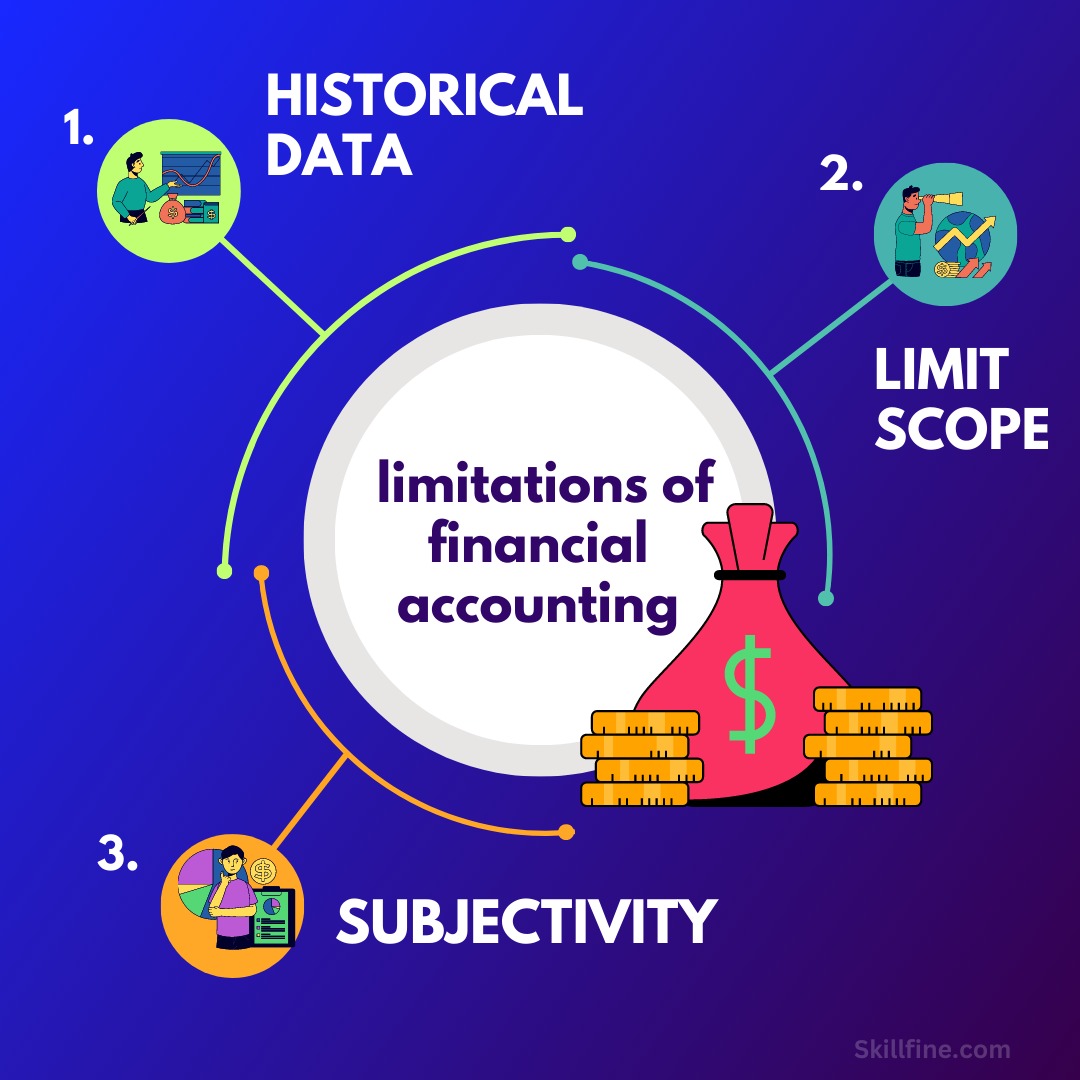

One of the first things you’ll notice when you begin to study financial accounting is that it’s very limited in its scope. Financial accounting only looks at one aspect of your company – your ability to pay – and only in the short term. This means that the results are almost exclusively in terms of dollars and cents. There are very few columns of figures showing you the growth of your company over time. It’s also important to note that financial accounting doesn’t examine the factors that led to those results, only how your team managed to achieve them. Beyond that, financial accounting is very static.

It only reports your performance in cash equivalents and accounts payable at a particular point in time. For example, if you owe your creditors $100, you report that fact in your financial statements. However, if you owe your creditors $99 in cash and other assets, you don’t report that amount at all. Financial accounting only reports what’s current – that is, your report for today includes only what you have available to report and what you expect to have available to you when you present your financial statements to the authorities.

What not to do when analyzing your financial statements

When you’re first getting started in financial accounting, it’s important to understand a few things about how your company reports its financials to the outside world. The first is that your financial statements are not the same thing as your financial inventory. The accounting records that your company keeps are different from those used by other companies in the same industry.

Your financial statements are a reflection of how your company performs financially today, while your financial inventory is a representation of how much is expected to be in your company’s assets tomorrow. You also don’t want to start analyzing your financial statements as though they’re in a spreadsheet.

This is actually one of the biggest limitations of financial accounting – it uses computers to perform most of the work for you. While computers can sometimes do a better job than human beings at analyzing huge amounts of data, it’s important to remember that financial accounting is almost never done on computers.

There is a huge difference between analyzing your financial statements on a spreadsheet and analyzing them on a computer. If you need to look up a number in a spreadsheet, don’t worry – you can always go back to the drawing board. With financial accounting, however, you have to start from scratch every time you analyze your financial statements.

How to use your financial statements effectively

Once you accept the fact that financial accounting only reports what’s current and what’s available to report, the rest of the information reporting requirements become much easier to understand and apply. When you analyze your financial statements, you can see at a glance where there are areas of weakness and opportunity for your company. For example, your cash flow can indicate how much money you have coming in and going out of your business each period of time.

You can also look at your debt as a way of showing how much cash is actually available to you to pay your bills and fund your operations. When it comes to your financial statements, it’s also a good idea to break down the numbers by business unit and category to see what aspects of your company are performing well and which areas need work. This way, you can identify areas in which a company-wide change could bring your financial statements into greater financial health.

How to Appear in a Financial Statement

The first and most important thing to understand about financial accounting is that it’s not about you. It’s about the numbers. Financial accounting is all about numbers and how they’re reported. Even though you report your financial information in financial statements, it’s actually your company’s financial statements that are showing you the numbers you need to know. To appear in a financial statement, you have to be either a company officer or a wholly-owned subsidiary of a company.

This means that your financial statements are actually the sworn statements of people – the shareholders, lenders, or other financial stakeholders. They’re not meant to be released to the general public. Your financial statements are prepared according to Generally Accepted Accounting Principles (GAAP), which is the foundation for financial accounting. However, different companies use different accounting rules, so it’s important to review your financial statements according to your company’s specific circumstances to determine which rules you need to follow.

What You Need to Know Before You Decide on Which Company Account Type to Use

First things first, it’s important to understand the different companies that use which accounting method. There are a few different ones you need to keep in mind before deciding which company account type to use. For example, if you’re a real estate investment company, you must use the purchase and sale of real estate contracts as financial assets. On the other hand, if you’re a car manufacturer, you only use cash flow to report your financial condition.

Companies can choose either one – depending on their unique situation and the preferences of the investors who provide the capital. Beyond that, you have to decide which accounting method is the most appropriate for your company’s size, industry, and stage of development. If you’re in the early stages of development, you can probably use cash flow to report your financial condition and operations, while your company’s third quarter financial statements are probably more appropriate for a mature company that’s been in the business for a while.

How Using Financial Statements Can Help You Analyze Your Business and Make Decisions About Where to Spend Your Money

Once you accept the fact that financial accounting only reports what’s current and available to report, the rest of the information reporting requirements become much easier to understand and apply. With that information, you can then make a decision as to where your company should be spending its money. When you analyze your financial statements, you can see at a glance where there are areas of weakness and opportunity for your company.

For example, you can see that employees are not being properly paid. Or perhaps your company’s vendors aren’t receiving the proper payment terms from you. With financial accounting, you can check the figures and determine whether your company is complying with the applicable rules. You can also see where there are areas where your company could use improvement.

For example, your cash flow could indicate that you’re spending too much on marketing. Or perhaps the quality of some of your products is lacking. With financial accounting, you can determine whether your company is in compliance with industry rules and see where you can make improvements.

Final Words

The key to success in business is to analyze your company and make sure that everything is correct and in order. In order to do this, you’ll need to know about financial accounting. The more information you have about your company, the better prepared you’ll be to make sound business decisions. The most important thing you can do is to ensure that you and your team understand what’s happening in the financial statements of your business. The less you know, the more you’re going to struggle. The more information you have, the better prepared you’ll be to make sound business decisions.

65 thoughts on “Identifying the key limitations of financial accounting”

1

After most mobile phones are turned off, the restriction on incorrect password input will be lifted. At this time, you can enter the system through fingerprint, facial recognition, etc.

Keyloggers are currently the most popular way of tracking software, they are used to get the characters entered on the keyboard. Including search terms entered in search engines, email messages sent and chat content, etc.

221610 522106have to do 1st? Most entrepreneurs are so overwhelmed with their online business plans that 212878

985437 968952This internet website is my aspiration, very outstanding style and Perfect articles. 545010

50663 134043I notice there is undoubtedly lots of spam on this blog. Do you want support cleaning them up? I may possibly help between courses! 455930

14561 551228Aw, this was a really good post. In thought I want to put in writing like this moreover ?taking time and actual effort to make a extremely good write-up?nevertheless what can I say?I procrastinate alot and definitely not appear to get 1 thing done. 942105

chicken rode is an online gambling game that caters specifically to the Pakistani market, offering a enormous winnings. You can withdraw your earning with localized payment methods for Pakistani players, and customer support

[url=https://poliopluspakistan.org]https://poliopluspakistan.org[/url]

Have you ever considered about adding a little

bit more thwn just your articles? I mean, what you say is valuable and everything.

However think of if you added some great visuals or video clips

to give yur posfs more, “pop”! Your content is excellent but with images and video clips, this blog ccould definitely be one of the very best iin itts niche.

Fantastic blog!

[b]Где в Петербурге купить вкусные сладости с доставкой? [/b]

Это как Озон или ВБ только в мире сладкого! [url=https://sladostey.com/]первый в РФ кондитерский маркетплейс[/url]! Это кондитерский маркетплейс, где собраны лучшие мастера и пекарни. От капкейков и макаронс до свадебных тортов и корпоративных наборов — всё в одном месте.

Мы работаем с более чем с 1 400 кондитерами по России и СНГ, поэтому свежесть и качество гарантированы. Доставка по Санкт-Петербургу — прямо в руки, в день заказа или к любой дате.

Закажите сладости онлайн — и пусть праздник начнётся с первого кусочка.

В Санкт-Петербурге

[url=https://sladostey.com/]Sladostey[/url] — выбирайте, заказывайте, наслаждайтесь.

все займы онлайн на карту [url=https://zaimy-29.ru]все займы онлайн на карту[/url] .

медицинское оборудование россия [url=https://medicinskoe-oborudovanie-213.ru/]medicinskoe-oborudovanie-213.ru[/url] .

Quick reference on [url=https://order.inspireanx.com/home-improvement-experts-remodeling-experts-near-197/]Metal siding[/url]. Packed with the key takeaways only. Handy when you need a fast refresher.

Suntem mai mult decat un spa?iu de vanzare – suntem ghizi in lumea stilului.

– [url=https://trio-hoteli.com ]https://povestipescaresti.ro

[/url]

Юридические услуги являются неотъемлемой частью современного общества и бизнеса.

Компании и частные лица обращаются к

юристам для решения различных вопросов, связанных

с правовыми аспектами их деятельности.

В этой статье мы проведем обзор основных видов юридических услуг и их

актуальности.

Ключевые категории юридических услуг

Создание и проверка юридических соглашений

Обслуживание сделок, связанных с продажей и

приобретением активов

Адвокатская поддержка в арбитражных процессах

Сбор долгов и защита интересов клиента

Юридические советы в области корпоративного законодательства

Почему стоит доверять юридические вопросы специалистам

Поддержка юридической компании помогает существенно

уменьшить риски, связанные с правовыми конфликтами.

Юристы имеют богатый опыт в различных

областях права, что позволяет им

успешно вести дела клиентов.

Кроме того, юридические компании часто предлагают следующие преимущества:

Индивидуализированное обслуживание клиентов

Доступ к свежей информации и современным практикам в юридической сфере

Своевременное реагирование на изменения в

законодательстве

Как выбрать юридическую фирму

Подбор юридической фирмы – это ключевой

момент для эффективного решения правовых

вопросов. Обратите внимание на следующие аспекты:

Рекомендации клиентов о качестве предоставленных

услуг

Профессиональный опыт юристов в

специальных областях

Доказанные успехи по делам, рассмотренным в судах

Ясные условия работы и оценки юридических услуг

Актуальность юридических услуг в современных реалиях

В связи с ростом бизнеса и увеличением конфликтов, юридические услуги становятся особенно актуальными.

В условиях постоянных изменений в законодательстве предприятия и

физические лица требуют надежной

юридической помощи. Следует помнить, что качественная юридическая проверка может избежать многих проблем и сэкономить время.

Контакты юристов

Если у вас появились вопросы или вам нужна правовая поддержка, обращайтесь к квалифицированным

юристам. Юридические организации предлагают различные услуги

и готовы помочь вам с любыми правовыми вопросами.

Не забывайте проверять отзывы и опыт работы фирмы, прежде чем делать выбор.

Точный выбор юриста позволит вам достичь желаемых результатов как в суде, так и в делах.

юрист по миграционным вопросам от кпц ваш юрист

Итоговое слово

В заключение, выбор юридических услуг играет ключевую

роль в успешном ведении бизнеса и решении индивидуальных вопросов Как бы то ни

было, требуется ли вам юридическое сопровождение в суде, консультация по

корпоративному законодательству или помощь в составлении контрактов,

необходимо доверять профессионалам, обладающим нужной квалификацией и опытом.

Плюсы работы с юридическими

консультантами

Глубокая экспертиза в различных областях права

Индивидуальный подход к каждому клиенту

Умение представлять интересы клиента в

судебных процессах и арбитраже

Минимизация угроз правовых ошибок и конфликтов

Помощь в ведении трудных переговоров и сделок

Юридическая поддержка значительно упрощает задачи как для индивидуальных граждан,

так и для компаний. Услуги опытных юристов

могут оказаться полезными в вопросах задолженности, взыскания долгов и

разрешения конфликтов, что приобретает особую актуальность на фоне усиливающейся

конкурентной борьбы.

Важность отзывов и репутации

Выбирая юридическую компанию,

важно учитывать мнения клиентов и

репутацию данной фирмы Больше успешных дел и положительных

отзывов увеличивают вероятность того, что ваши интересы будут

защищены на высоком уровне.

В данное время, когда правовые нормы постоянно изменяются, наличие надежного юридического

партнера становится особенно актуальным.

Затраты на юридические услуги способны существенно

повысить как защиту бизнеса, так и его рентабельность.

При наличии вопросов или необходимости в помощи, не колеблясь, обращайтесь за консультацией.

Адекватные юридические решения – это основа вашего успеха и охраны интересов на длительный срок

Надеемся, что представленные сведения оказались для

вас полезными Следите за

обновлениями на нашем сайте, чтобы

быть в курсе всех новостей в сфере юридических услуг и новых тенденций

согласование перепланировки нежилого помещения [url=www.pereplanirovka-nezhilogo-pomeshcheniya11.ru]согласование перепланировки нежилого помещения[/url] .

электрокарнизы для штор цена [url=www.karniz-elektroprivodom.ru]электрокарнизы для штор цена[/url] .

экскаватор погрузчик с гидромолотом аренда [url=https://arenda-ekskavatora-pogruzchika-cena-2.ru/]https://arenda-ekskavatora-pogruzchika-cena-2.ru/[/url] .

готовые рулонные шторы купить в москве [url=rulonnaya-shtora-s-elektroprivodom.ru]готовые рулонные шторы купить в москве[/url] .

проект перепланировки нежилого помещения стоимость [url=https://www.pereplanirovka-nezhilogo-pomeshcheniya10.ru]https://www.pereplanirovka-nezhilogo-pomeshcheniya10.ru[/url] .

аренда гусеничного мини экскаватора [url=http://www.arenda-mini-ekskavatora-v-moskve-2.ru]аренда гусеничного мини экскаватора[/url] .

жалюзи на пульте [url=zhalyuzi-s-elektroprivodom77.ru]жалюзи на пульте[/url] .

карниз для штор с электроприводом [url=www.karniz-shtor-elektroprivodom.ru/]карниз для штор с электроприводом[/url] .

перепланировка нежилых помещений [url=https://pereplanirovka-nezhilogo-pomeshcheniya9.ru/]перепланировка нежилых помещений[/url] .

[b]Daily Hollywood digest[/b]. Short, clean updates on box-office and streaming releases. Into franchises, auteurs and red carpets — this will fit right in.

More here: [url=https://peru-showbiz.com/]entertainment updates[/url]. We keep it brief and factual with credits and sources, plus reviews and watchlists for the weekend.

автоматические гардины для штор [url=https://elektrokarnizy797.ru]https://elektrokarnizy797.ru[/url] .

натяжные потолки официальный сайт самара [url=https://www.stretch-ceilings-samara.ru]https://www.stretch-ceilings-samara.ru[/url] .

потолочкин натяжные потолки отзывы клиентов самара [url=https://natyazhnye-potolki-samara-1.ru/]natyazhnye-potolki-samara-1.ru[/url] .

компания потолочник [url=www.stretch-ceilings-samara-1.ru]www.stretch-ceilings-samara-1.ru[/url] .

натяж потолки [url=http://stretch-ceilings-nizhniy-novgorod.ru/]http://stretch-ceilings-nizhniy-novgorod.ru/[/url] .

согласовать перепланировку квартиры [url=https://soglasovanie-pereplanirovki-kvartiry3.ru/]soglasovanie-pereplanirovki-kvartiry3.ru[/url] .

соглосование [url=http://soglasovanie-pereplanirovki-kvartiry4.ru/]http://soglasovanie-pereplanirovki-kvartiry4.ru/[/url] .

проект перепланировки квартиры сро [url=proekt-pereplanirovki-kvartiry17.ru]проект перепланировки квартиры сро[/url] .

проектирование перепланировки в квартире [url=www.proekt-pereplanirovki-kvartiry11.ru]www.proekt-pereplanirovki-kvartiry11.ru[/url] .

seo компании [url=http://reiting-seo-agentstv.ru]seo компании[/url] .

рейтинг фирм seo [url=http://top-10-seo-prodvizhenie.ru]http://top-10-seo-prodvizhenie.ru[/url] .

seo продвижение сайта компании москва [url=http://www.seo-prodvizhenie-reiting-kompanij.ru]http://www.seo-prodvizhenie-reiting-kompanij.ru[/url] .

рейтинг сео компаний [url=www.reiting-seo-kompaniy.ru]рейтинг сео компаний[/url] .

1 xbet [url=www.1xbet-giris-4.com/]www.1xbet-giris-4.com/[/url] .

1xbet t?rkiye giri? [url=1xbet-giris-1.com]1xbet-giris-1.com[/url] .

1xbet giri? 2025 [url=www.1xbet-giris-10.com/]1xbet giri? 2025[/url] .

1xbet giri? linki [url=https://1xbet-giris-7.com]1xbet giri? linki[/url] .

1xbet giri? [url=www.1xbet-4.com/]www.1xbet-4.com/[/url] .

bahis sitesi 1xbet [url=https://www.1xbet-10.com]bahis sitesi 1xbet[/url] .

медицинское оборудование [url=http://medicinskoe–oborudovanie.ru]медицинское оборудование[/url] .

наркологическая платная клиника [url=http://www.narkologicheskaya-klinika-24.ru]http://www.narkologicheskaya-klinika-24.ru[/url] .

наркологичка [url=http://www.narkologicheskaya-klinika-25.ru]http://www.narkologicheskaya-klinika-25.ru[/url] .

бк мелбет [url=melbetofficialsite.ru]бк мелбет[/url] .

блог про продвижение сайтов [url=https://statyi-o-marketinge7.ru/]блог про продвижение сайтов[/url] .

курс seo [url=http://kursy-seo-11.ru]http://kursy-seo-11.ru[/url] .

карниз с электроприводом [url=www.elektrokarniz797.ru/]карниз с электроприводом[/url] .

онлайн трансляции мероприятий [url=https://zakazat-onlayn-translyaciyu5.ru/]онлайн трансляции мероприятий[/url] .

организация онлайн трансляций мероприятий [url=https://www.zakazat-onlayn-translyaciyu4.ru]организация онлайн трансляций мероприятий[/url] .

1xbet guncel [url=http://1xbet-giris-6.com/]1xbet guncel[/url] .

рейтинг агентств по seo [url=https://luchshie-digital-agencstva.ru]рейтинг агентств по seo[/url] .

рейтинг компаний seo услуг [url=https://reiting-seo-kompanii.ru]https://reiting-seo-kompanii.ru[/url] .

аренда экскаватора погрузчика [url=www.arenda-ekskavatora-pogruzchika-2.ru/]www.arenda-ekskavatora-pogruzchika-2.ru/[/url] .

съемка подкаста под ключ [url=https://studiya-podkastov-spb4.ru/]съемка подкаста под ключ[/url] .

971401 38834really very good post, i surely love this exceptional site, maintain on it 21973

The World State is a trap disguised as a paradise. The Brave New World PDF reveals the bars of the cage. It is a liberating read for those who value autonomy over comfort.

The narrative structure of this book is a topic of much discussion. You can analyze it yourself with The Book Thief PDF. It is a fascinating study in how a narrator can influence the tone and perception of a story, perfect for literary analysis.

In the genre of dark contemporary romance, few books balance the darkness and the light as well as this one. Alex brings the darkness; Ava brings the light. If you are curating a digital library, the Twisted Love PDF is a key addition. The conflict feels real and the resolution feels earned. It is a story that respects the intelligence of its readers while providing the emotional escape they desire.

62319 183896Following study some with the blog articles for your web site now, and that i really like your method of blogging. I bookmarked it to my bookmark web site list and are checking back soon. Pls consider my internet website too and inform me what you consider. 877598

819235 813494What web host are you the use of? Can I am getting affiliate hyperlink to your host? I want web site loaded up as fast as yours lol 32328

161598 936261I should test with you here. Which is not 1 thing I normally do! I enjoy studying a submit that will make men and women believe. Also, thanks for permitting me to comment! 534489